Lars Tranberg from Danske Bank said European banks are reduced to borrowing dollar funds for "a week at a time" rather than the usual six to 12 months. "This closely resembles what happened in late 2008, though the difference this time is that the major central banks have dollar swap lines in place. If the dollar funding markets completely freeze up, the European Central Bank can act as a backstop."

Mr Tranberg said dollar deposits of US banks have increased by $400bn since mid-June, mostly offset by dollar reductions in Europe. "It is clear that the problem lies with the European banks. The credit default swaps on these banks are very high and provide a risk gauge."

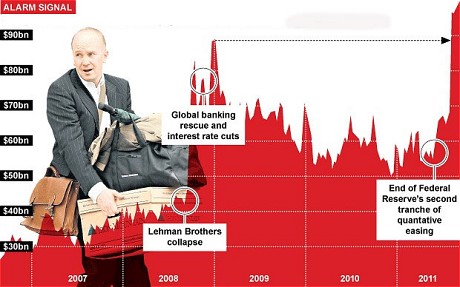

The Bank for International Settlements says European and British banks have a dollar "funding gap" of up to $1.8 trillion stemming from global expansion during the boom that relies on dollar financing and has to be rolled over. This is not normally a problem but funding can seize up in a crisis.

European officials hotly disputed claims in a leaked document from International Monetary Fund claiming that a realistic "mark-to-market" of Italian, Spanish, Greek, Irish, Portuguese and Belgian sovereign debt would reduce the tangible equity of Europe's banks by €200bn (£176bn).

"French banks passed stress tests which were extremely tough less than a month ago: there is no cause for worry," said Valerie Pecresse, France's budget minister.

"It is ill advised to provoke alarm," said Michael Kummer, head of Germany's BdB bank federation.

The IMF was attacked as a Cassandra when it warned early in the credit crisis that debt write-downs would reach $600bn, yet losses have since reached $2.1 trillion.

European banks are still struggling to access America's $7 trillion money market funds. Fitch Ratings said last week that Spanish and Italian banks have been cut off altogether.

Investors do not fully believe EU pledges that the 21pc "haircut" agreed for private holders of Greek debt is the end of the story, or will remain confined to Greece, as the second Greek rescue is already unravelling. A Greek parliament report concluded that deep recession is pushing the country into a downward spiral, causing debt dynamics to fly "out of control". Public debt will reach 172pc of GDP next year.

Simon Derrick from BNY Mellon said Germany, Holland, and Finland may balk at a third rescue in the current tetchy mood, implying bigger haircuts instead. That will set a precedent for Portugal, and others. Until markets can see an end to the blood-letting, Europe's banks will remain untouchables.

By Ambrose Evans-Pritchard

Source > Telegraph